New Stock! The Next Big Leap in Memory Technology... (and Profits)

Welcome to the June edition of the newsletter!

In Russia, there’s a long-forgotten place that looks about as bleak as its name…

Akhmatov’s Pit.

Located in Russia’s desolate Ural Mountains, it’s hard to believe that the crystallized mineral first discovered in this ancient quarry in 1836 is responsible for the next stage of the semiconductor revolution.

Watch and listen to the video, or read on for more details!

But Airbus recently started using new chips based on it in their jets. BMW is installing similar chips in their vehicles.

Companies as diverse as Cisco, Intel, Honeywell, Motorola, Dell Technologies, and iRobot (maker of the Roomba robotic vacuum cleaners) among many others - have all embraced the technology as well.

In fact, this particular part of the chip industry is growing at a rate of more than 30% a year.

At that pace, it will mushroom in size from a $400 million industry (in 2019) to a $12 billion market by 2030.

So in terms of market opportunities, we’re talking Nvidia when it launched its first gaming chips in 1999, Intel with its early microprocessors in 1970, and Texas Instruments when it started mass producing transistors in 1951.

That kind of growth.

And it all started 185 years ago with a prospector and mineralogist named Gustav Rose.

While digging at Akhmatov’s Pit, he found these weird crystals, shaped like little black sugar cubes.

Turns out no one had identified them before.

Rose named the crystals “perovskites” (in honor of a helpful bureaucrat and benefactor in the Czar’s government back in St. Petersburg).

Gustav Rose’s revolutionary discovery went into the geology journals of the era.

And then?

Nothing. Rose’s new crystal was promptly ignored and forgotten by his fellow rockhounds.

But 150 years later, something amazing happened.

In the 1980s, 2 researchers discovered that perovskites – now synthesized in a laboratory - are natural “superconductors.” Electricity flows through the crystal with almost zero resistance at room temperature.

Just think of the possibilities, like hyper-efficient solar panels.

The discovery won them the 1987 Nobel Prize for Physics.

Around the same time, 2 other researchers had their own “Holy Cow!” moment…

Turns out perovskites can alter & control the “spin” of electrons. If “spun” in the right direction, electrons can even create “microcells” of magnetism.

It took 20 years, but those 2 scientists won their own Nobel Prize for Physics in 2007.

In academic journals, they call their discovery “GMR” – giant magneto-resistance.

But quickly, an alternative term was coined to describe this emerging technology…

The Birth of Spintronics

Spintronics sounds odd when you say it out loud.

But it makes sense if you think about it.

Electronic computing is all about electrons (or the absence of them). The circuits printed on a computer chip are either on or off, 1’s and 0’s, right?

Spintronic computing generates 1s and 0s as well — but by manipulating the spinning direction of the electron, and thereby inducing magnetism (or not) in the cells/circuits of a chip.

You can see where this is going…

For example, as many of us experience all too often, digital electronics become unstable and slow at the worst possible times.

- Computer chips get too hot and lose their processing power.

- A lightning bolt zaps the phone pole outside and corrupts your hard drive.

- Even the smallest wireless iOT sensors guzzle battery power.

- Radiation in outer space is the biggest cause of failure and degradation of digital electronics.

Spintronic-based components sidestep all of that.

We’re talking chips that generate far less heat.

Sensors that need practically no power to be “on” at all times.

Un-corruptible memory chips and drives that read/write data much faster.

That technology is starting to become commercially available. Not next year or 5 years. But right now.

The leading player in this burgeoning corner of the chip industry is the focus of this month’s newsletter, Everspin Technologies (MRAM).

As tech companies go, Everspin is no startup.

The company had its IPO in 2016. But its roots go back to 2008, when Everspin was “spun” out of its corporate parent, Freescale Semiconductor.

At the time, spintronics and its base technology - MRAM (magnetoresistive random access memory) was more of a lab project than a business.

But since its founding, EverSpin has been awarded more than 400 patents for information storage innovations.

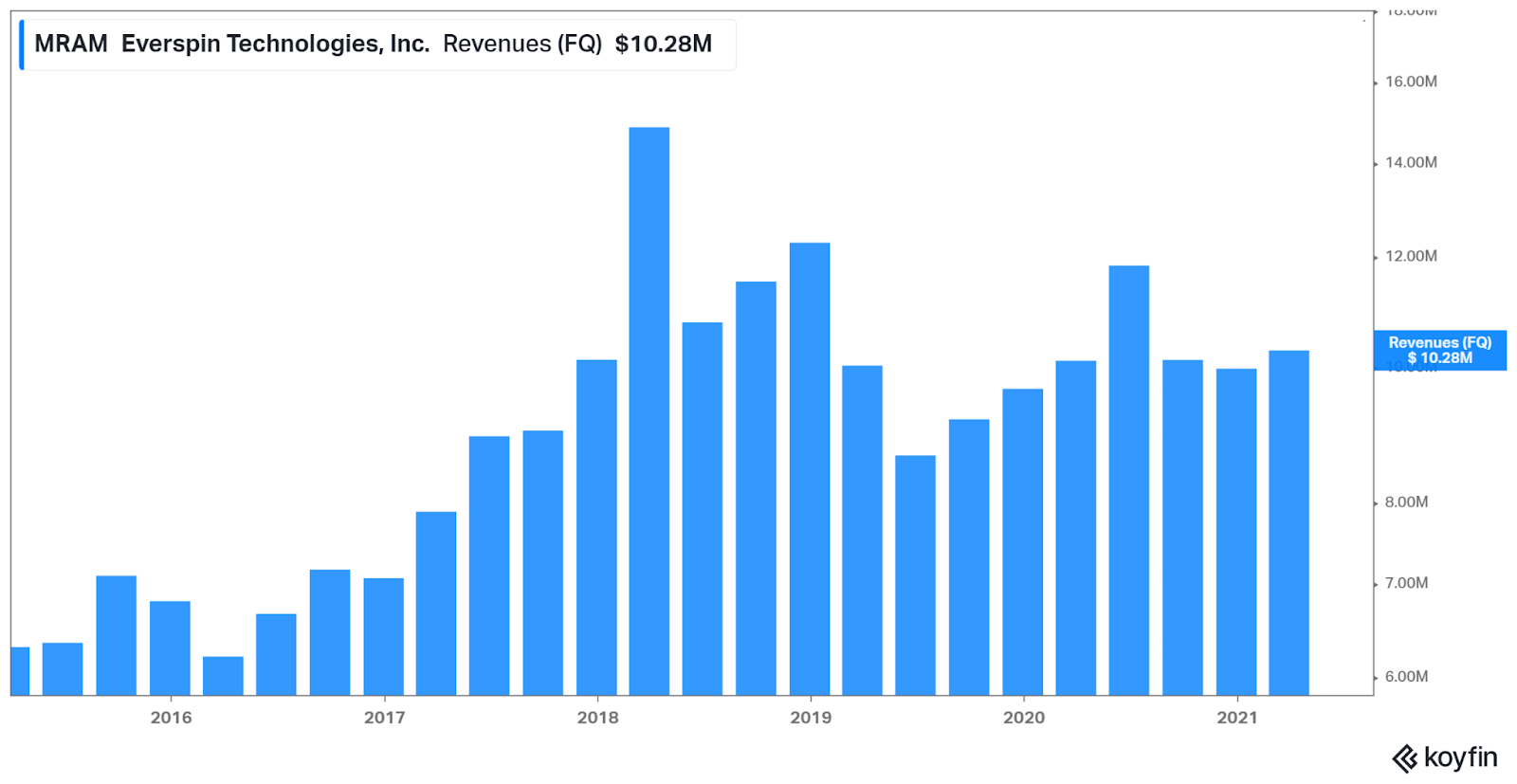

By 2015 though, the technology was mature enough to hit the commercial market; EverSpin generated revenue of nearly $26 million.

As you can tell from the chart, the demand for Everspin’s MRAM-based memory chips has been building in a slow, sustainable manner.

But I think it’s about to explode in a dramatic fashion.

See, the big data, computer and networking companies are the major purchasers of memory chips. For them, until recently, MRAM technology was sort of like owning an exotic supercar to get around town, when a 4 cylinder subcompact did the job just as well - and much cheaper.

For years, these companies have relied on components incorporating older technologies like DRAM (dynamic random access memory) and so-called flash RAM.

But we’re converging on a new tech world.

Hyperconnectivity is the goal.

The big telecom firms are building out their superfast 5G data networks. Companies of all kinds are creating the “internet of things” by equipping their factories, offices, and products with arrays of sensors that pump out rivers of data day and night.

Even for regular folks like us, when we stream Netflix the last thing we want to see is one of those annoying, spinning “buffering” symbols on our video screen. We expect our data to always be there, as soon as we need it.

But it’s getting harder for tech companies to fulfill those expectations when using older memory technology.

For instance, computer chips of all kinds generate lots of heat. Cooling costs are a major expense for data center operators.

So is assuring the reliability and stability of computer data, and “backing up” that data in case there’s a problem.

Lastly, the internet of things is creating massive demand for sensors - which drink steady quantities of electricity from a battery or other power source.

For product designers, there’s also a circuit board “real estate” problem. Even a tiny dime-sized “watch battery” or capacitor (a type of chip that can store a charge of electricity) takes up valuable space, meaning the overall sensor package itself has to be made that much larger.

So here’s where Everspin and its MRAM technology joins the party.

As the largest (by far) manufacturer of MRAM chips, the company is in an ideal position, with the right product at the right time - especially as we move towards a more normal post-pandemic global economy.

I’ve already shown you Everspin’s quarterly revenue chart to date. But analysts are expecting the company to finish 2021 with sales of nearly $46 million (up 9% from last year’s pandemic-slowdown and a stone’s throw from the company’s alltime record of $49 million in 2019. Analysts expect sales to rise nearly 20% next year, to nearly $54 million.

But there are 2 other fundamentals to Everspin that I like.

Path to Profits

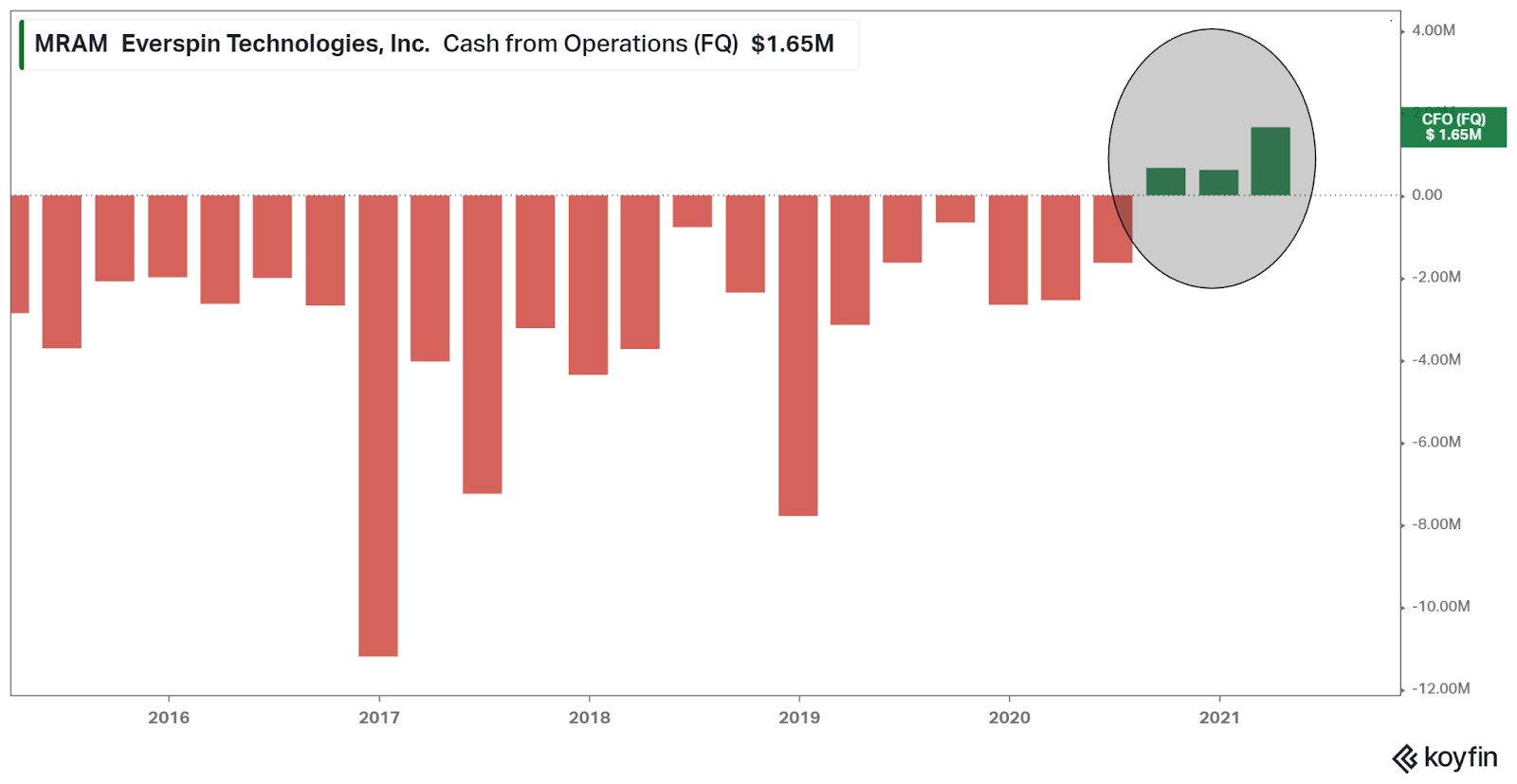

One is that even with last year’s sales slowdown, the company hit a remarkable milestone by notching its third consecutive quarter of positive cash flow.

That’s hugely important.

It means Everspin has plenty of demand for its products, and that those products command a strong premium from buyers in a very competitive marketplace.

It also means that, unlike many younger tech companies, Everspin no longer needs to borrow (or sell more shares of stock) to meet its immediate needs for salaries and other routine operational costs.

In my experience, young companies that are historically “cash positive” and “cash rich” can grow at a stable, sustainable pace for years on end - and often go on to dominate their industries.

Everspin’s other fundamental is the most important of all for stock investors like us - a path to profitability.

Cutting to the chase, the company surprised Wall Street analysts last month when it posted its first-ever quarterly profit of 1 penny a share (after losing a nickel a share in the same quarter a year ago, and recording a loss of 21 cents a share in Q1 of 2019).

I think there’s a lot more where that came from. While analysts expect a series of mild quarterly losses for the remainder of the year (with a total loss of $0.03 a share for 2021), I think they could be vastly underestimating the growth of Everspin’s business this year.

Likewise, they expect a mushrooming in growth in 2022, and see the company earning profits of $0.27 a share next year.

But again, they may need to dramatically “up” their estimates in coming quarters if Everspin’s performance in the first quarter of this year is any indication.

If I’m right, then Everspin (in my opinion) has a shot at rising 50% between now and the end of the year, and perhaps doubling or even tripling over the next 18 months.

We can figure that out with a little bit of painless math and the use of a handy measure of a stock’s value - a matric called a price/earnings (P/E) ratio.

If we take a stock’s share price and divide by its annual earnings per share, we generate a P/E ratio.

So if we divide Everspin’s current stock price of $6 by its expected earnings per share next year (of $0.27 a share), we get a p/e ratio of 22.

That’s far too low.

By comparison, the premier chip company these days - Nvidia (NVDA) - carries a price/earnings ratio of 47!

I’m betting that we’ll see something similar happen with Everspin Technologies as the stock proves itself to Wall Street, more investors become aware of the company, what it does, and its rapid growth.

If we reverse our math, and apply a P/E ratio of 47 to Everspin’s profits of $0.27 a share next year, it would predict a stock price of nearly $14 a share for the company.

Mind you, investors sometimes bid stocks to even higher levels (and higher p/e ratios) on the expectation of enormous, rapid profits. That’s why I say a tripling of the stock price to $18 by sometime next year isn’t out of question.

Everspin Technical Analysis

Between now and then though, we have one question mark - the technical path forward for the stock...

Keep in mind, I’m putting Everspin into the tracking portfolio now. I think it’s buyable right now.

But the chart below roughly sketches out two potential paths for the stock over the next handful of months.

My hoped-for expectation (the blue line) is that the stock is just about the break out of a longstanding “triangle” formation and work its way higher as the economy improves and investors look for new tech stock ideas that haven’t already been bid to the sky.

But there’s also a chance that the stock could remain trapped (the dotted red line) within the triangle through the summer, especially if the Nasdaq weakens.

Triangle formations like the one below are common enough. They have zero predictive value. But if enough traders draw them on their charts (as I have), well, they have a way of defining the path of least resistance for a stock.

So even though Everspin’s shares burst higher in recent weeks (which I’ve circled below), there’s a possibility that we could see the stock once again deflate back towards the $4 or $5 level as the stock bides it's time until the upper and lower parts of the “triangle” converge somewhere in September or October.

Let’s also remember that investing in any stock, no matter how promising it appears, always carries a degree of risk. It’s our job as investors to assess whether there’s enough potential reward to compensate us for the potential risk as well.

Stocks can and do fall dramatically, often when we least expect.

But that said, I continue to like the picture being painted by Everspin Technologies, both as a stock, and as a business. This is a good time, in my opinion, to be adding it to the portfolio.

Best of Good Buys,

Jeff

Member discussion